PELICE is the Educational Event for the Worldwide Wood Products Industries Including Veneer, Plywood, OSB, MDF, Particleboard, Engineered Wood Products, Mass Timber and Value Added

PELICE Speakers Addressed Everything From AI To Wood Supply

EDITOR’S NOTE: This is the second part in a series of articles covering the 2026 Panel & Engineered Lumber International Conference & Expo (PELICE) held April 16-17 at the Omni Hotel in Atlanta. The event, hosted by Panel World and Georgia Research Institute, featured 470 registrants, 95 exhibitors, 41 speakers and attracted representatives from 25 wood products producer companies.

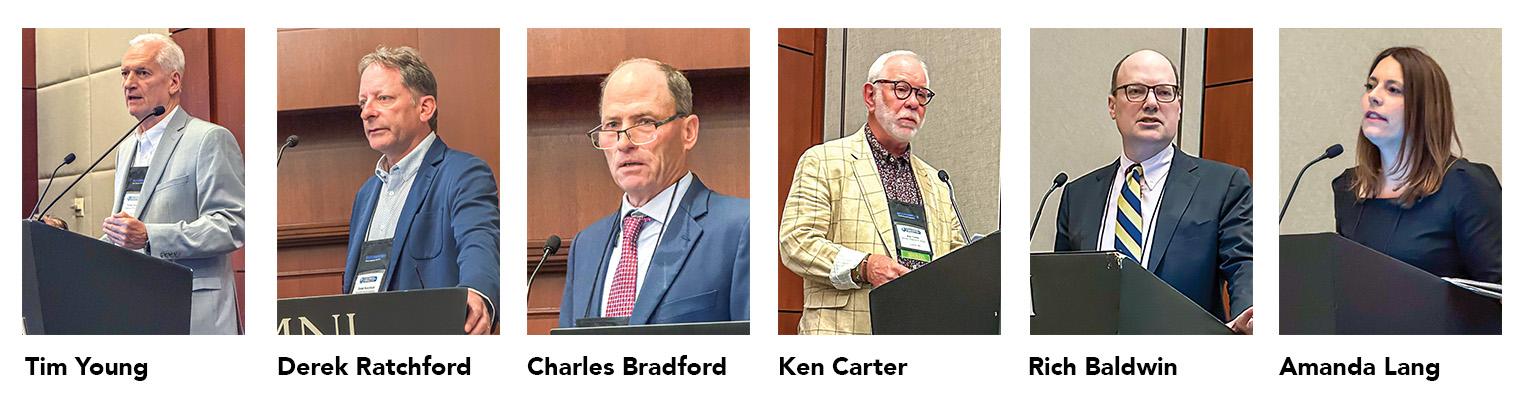

“How Machine Learning and AI (Artificial Intelligence) Will Transform the Leading Companies of the Panel Industries” was the title of the presentation delivered during the second morning keynote session by Tim Young, professor emeritus and interim director of the Data Science Institute at the University of Tennessee.

Young has spoken at previous PELICE events about the establishment of Digital Twin and the coming of AI, and his earlier projections appear to be hitting the nail on the head today.

Young indicated that the discussions around AI have moved into an adaptive phase, and companies should have an investment (and leadership) commitment in place and moving into implementation—if not already there. For example, he said, AI systems or reasoning models can process and solve certain software issues with a tremendous success rate that humans would require 20 minutes to locate, evaluate and fix, representing a tremendous leap in AI capability even in the past year.

Young referred to the AI Ecosystem and described the different habitats that comprise it, from reactive machines to Machine Learning, neural networks, narrow AI, and limited memory to self-aware AI and super-intelligent AI.

“Machine Learning algorithms are replacing human-written ladder logic in PLCs,” Young said.

He said AI is transforming business systems because of less variation and less cost through statistical and probabilistic demand forecasting, optimized supply planning, real-time decision logistics and execution, and predictive and prescriptive risk management.

Young added that AI has enhanced predictive maintenance, prescriptive maintenance and now-emerging autonomous maintenance when systems self-diagnose and trigger actions in integration with control systems and robotics for example.

“For businesses and production systems, Machine Learning and AI will be essential for success,” Young said, adding that people need to overcome the ML & AI literacy problem, but the question persists: “Will humans continue to learn, and at what rate?”

Derek Ratchford, CEO of SmartLam North America, told of that company’s production growth in mass timber, through a joint ownership of several well known sawmill companies, including Two Rivers Lumber, Collum’s Lumber, Charles Ingram Lumber and Rex Lumber. Several years ago the company committed to the investment of $85 million toward upgrading automation at its CLT facilities at Columbia Falls, Mont. and Dothan, Ala., and for the construction of a greenfield glulam facility in Dothan.

Ratchford said several key factors came together to drive the investment. He said the market was ready; that mass timber had successfully “crossed the chasm” from a niche production into a high-growth mainstream market; SmartLam had established itself as a solid performer, earning the confidence of the ownership group; capital was available through the strong financial position of the ownership especially following the prosperous “Covid” years; and the fact that the company’s existing CLT plants were operating at maximum capacity, creating a bottleneck for future growth.

Ratchford said the “secret sauce” to the successful implementation of the investment projects has been its people, providing expertise at every step, including in-house engineering & modeling and precision execution, on an operational philosophy of growing talent from within through continuous cross-training.

Where does SmartLam go from here? Ratchford said its vision is to evolve from a project-based approach to leading the market with “productized solutions,” developing core and shell building systems that are ready-to-assemble, meeting the needs of developers while leveraging the company’s production efficiencies.

Charles Bradford, VP of Procurement at Scotch Plywood, and Ken Carter, VP at Winston Plywood & Veneer, gave respective presentations in the Catastrophe Management session.

Bradford, in his talk “From Ashes to Operations,” reflected on the fire that took out the veneer mill in Waynesboro, Miss. in early 2021. Fortunately, there were no injuries, though the mill was a total loss.

While a lot of questions and uncertainties immediately surfaced, there was no hesitation from the family ownership at Scotch Plywood to move fast, including busing employees 120 miles to another company facility at Beatrice, Ala., maintaining production, customers and the supply chain, and moving forward on a total rebuild.

The rebuild at Waynesboro took 14 months and production records came shortly thereafter.

Bradford focused on the importance of insurance coverage for the building, machinery & equipment, business interruption and extra expenses, enabling immediate cleanup, continued operations, workforce retention and rebuild execution. The claim paid more than $40 million, according to Bradford, who gave a shout-out to MarshMcLennan Agency and its VP of Forestry & Wood Products Practice, Mike McCoy.

And then it happened again, Bradford said, this time a fire at the Beatrice facility on November 2, 2025, due to an electrical issue with the veneer chipper. No one was injured, but the green end was destroyed.

Bradford said Scotch has quickly implemented a “reverse model,” now increasing operations at Waynesboro and transferring logs from Beatrice to Waynesboro and shipping veneer from Waynesboro to a new dryer at Beatrice.

“What matters most?” Bradford asked. “Decide quickly. Protect your people. Maintain the system. Insurance. Going to 24/7. Execute and adjust.”

Carter of Winston Plywood & Veneer spoke on “Tribulation to Triumph (A Plywood Journey).” He showed a video and recalled when an F4 tornado struck Louisville, Miss. in spring 2014 and completely destroyed the plywood mill (while killing 10 and injuring 80 in the community). Ownership at Atlas Holdings broke ground on a new mill in early 2015, so the mill has been in operation for 10 years.

“Our story is more than a timeline of events,” Carter said. “It’s a story about people, purpose, and what it looks like to get knocked down and choose, together, to get back up.”

Carter noted that after 10 years of production, the mill is producing more than 7.5MMSF (3⁄8 in. basis) of plywood and veneer per week, and they’ve achieved a four-year run without a serious accident, and one minor incident over the previous 18 months.

Carter emphasized the many challenges the operation encountered, including building and operating a facility initially with mostly used equipment, and of hiring and developing a production team that was lacking in manufacturing experience, a reality that showed up in high turnover.

But perhaps the biggest challenge, or “opportunity” as Carter called it, was safety. For example, lockout/tagout was in place, but some employees were taking shortcuts, and hard decisions were made to terminate several employees for LOTO violations. “We doubled down on training. We worked to build a culture where anyone could stop the line if something wasn’t right.”

In the past 10 years Carter said they’ve invested more than $35 million in capital improvements for equipment and production lines, meanwhile developing a strong team of plywood professionals. Turnover rate has dropped significantly, thanks in part to a mentoring approach called “Pals Program.”

As they move forward, Carter said they continue to look at new automation technologies such as AI and robotic integration, but with caution. “What we’ve experienced so far (dealing with veneer and plywood) are all the variables of mother nature within the tree itself such as moisture, sap, density, etc. Where in automotive, for example, you’re dealing with a stamped part made of metal or plastic that’s exactly the same every time.”

Winston Plywood & Veneer is on “the road to 10 million,” Carter said. “Don’t be like the naysayers 10 years ago who told us we would never make a sheet of plywood.”

Rich Baldwin, principal consultant of Risk Advisors, provided a two-part presentation—the first part on the current state of the industry in North America.

He addressed the numerous challenges facing the structural wood products industry as of the first quarter—pricing dip in 2025 followed by marginal improvement in early 2026; permanently higher operating costs; relatively weak housing starts; a weak “macroeconomy” (inflation, mortgage interest rates, personal income, unemployment); unpredictable changes to foreign trade policies; weak profitability of forest products producers.

He also spoke on the state of the European Union Deforestation Regulation (EUDR), which the EU is enacting with the goal of limiting cutting of natural forests, and compels all wood and wood-related imports to the EU to comply with a due diligence checklist that includes the geographic location and harvest dates of all trees incorporated into those wood products—which is the most vexing requirement.

In December 2025, EU delayed implementation for large producers for one year to allow additional time to roll out IT systems. However, amending EUDR to include a “no-risk” category with minimal reporting requirements, which presumably would include the U.S. and Canada, has repeatedly failed.

Baldwin also addressed the growing Japanese influence in North America housing, and said it’s following a similar pattern of Japan’s influx into NA with automobiles, consumer electronics and steel. He cited investment in North America in building materials from companies such as Itochu and Sumitomo Forestry Corp., and in homebuilding from Daiwa House, Sekisui and Sumitomo. Also, Baldwin noted, the likes of machinery manufacturers Hashimoto Denki, Meinan, and Taihei have increased their participation in North American panel and engineered wood products operations.

Several reasons account for Japan’s focus on the U.S.—the Japan population and associated need for housing and building materials is decreasing, while the U.S. population and needs are increasing; Japanese businesses now have decades of experience becoming accustomed to U.S. culture and business practices; Japan’s Ministry of Land, Infrastructure, Transport & Tourism is emphasizing overseas growth of homebuilders and building materials with the U.S. as one of the primary targets.

Amanda Lang, president and COO of Forisk Consulting, spoke on fiber and timber supply and outlook. She said total capacity of U.S. wood-using pulp mills declined 26% over the past 11 years, representing 19 million tons lost, and that this shift of pulp demand is related to reduced demand for certain paper end products; increased use of recycled pulp; and increased efficiency in the production of paper.

Sawmill residual chips account for 33% of fiber demand in the U.S. by pulp, panel and pellet mills, according to Lang, who added that wood fiber users in the Western U.S. use 88% sawmill residual chips in their mix versus 25% in the U.S. South.

She noted that forest inventory in the U.S. South is 90% larger than it was in the early 1990s, and forecasts suggest that pine inventory will grow 1.7% per year in the next 10 years, and the most recent outlook has 4% more growth over 10 years than last year’s model due to mill closures.

PELICE 2026 in Atlanta: Industry Leaders, Big Investments, And A Clear Path Forward

The 10th Panel & Engineered Lumber International Conference & Expo (PELICE) lived up to its reputation as a can’t-miss industry event, bringing 470 attendees, 95 exhibitors, and 41 speakers to Omni Atlanta Hotel at Centennial Park on April 16–17.

The 10th Panel & Engineered Lumber International Conference & Expo (PELICE) lived up to its reputation as a can’t-miss industry event, bringing 470 attendees, 95 exhibitors, and 41 speakers to Omni Atlanta Hotel at Centennial Park on April 16–17.

Co-hosted by Panel World and Georgia Research Institute, the biennial conference—first launched in 2008—offers a timely pulse check on the panel and engineered lumber industries. The 2026 edition reinforced that role, delivering a mix of market realism, strategic clarity, and forward-looking optimism.

PELICE’s milestone 10th event carried added significance, including recognition of 18 exhibitor companies that have participated in all 10 conferences. Co-Chairmen Rich Donnell and Fred Kurpiel reflected on the event’s origins, with Kurpiel credited for first envisioning the conference and partnering with Panel World nearly two decades ago.

The audience included representatives from 25 producer companies, with executive leadership on hand to address a rapidly evolving business environment.

PERFECT 10 EXHIBITORS AT PELICE

The recent Panel & Engineered Lumber International Conference & Expo (PELICE), held in mid-April at the Omni Hotel in Atlanta, was the 10th PELICE since its inception in 2008. Event hosts Panel World magazine and Georgia Research Institute presented awards to 18 exhibitor companies that have participated in each PELICE. The Perfect 10 awards went to: Andritz, Con-Vey, Dieffenbacher, Dürr, Evergreen Engineering, Electronic Wood Systems, Flamex, Globe Machine, GreCon, Hexion, IPCO, Mid-South Engineering, Raute, Siempelkamp, TSI, USNR, Wechsler Technologies and Westmill.

Leadership Perspectives: Strategy, Culture, and Discipline

Georgia-Pacific: Building Value Through People

David Neal, Executive Vice President of Building Products, Georgia-Pacific, opened with a message centered on culture and long-term value creation.

David Neal, Executive Vice President of Building Products, Georgia-Pacific, opened with a message centered on culture and long-term value creation.

Neal emphasized the company’s “Principle Based Management” framework, rooted in stewardship and human progress, noting the importance of internal development and external relationships: “Building relationships and trust” remains fundamental to both business success and community impact.

He highlighted employees who rose through the organization, reinforcing how long-term investment in people translates into stronger partnerships and evolving customer solutions.

Boise Cascade: Staying Focused in a Volatile Market

Rob Johnson, Senior Vice President of Manufacturing Operations at Boise Cascade, addressed the company’s evolution into one of North America’s largest producers of engineered wood products.

Rob Johnson, Senior Vice President of Manufacturing Operations at Boise Cascade, addressed the company’s evolution into one of North America’s largest producers of engineered wood products.

Despite market pressures, Boise has resisted broad diversification, instead leaning into its core strengths: “We are an EWP-focused business. We consider plywood a byproduct of strength-rated veneer production.”

Johnson also pointed to the company’s integrated distribution model as a stabilizing force, helping smooth financial performance across fluctuating markets.

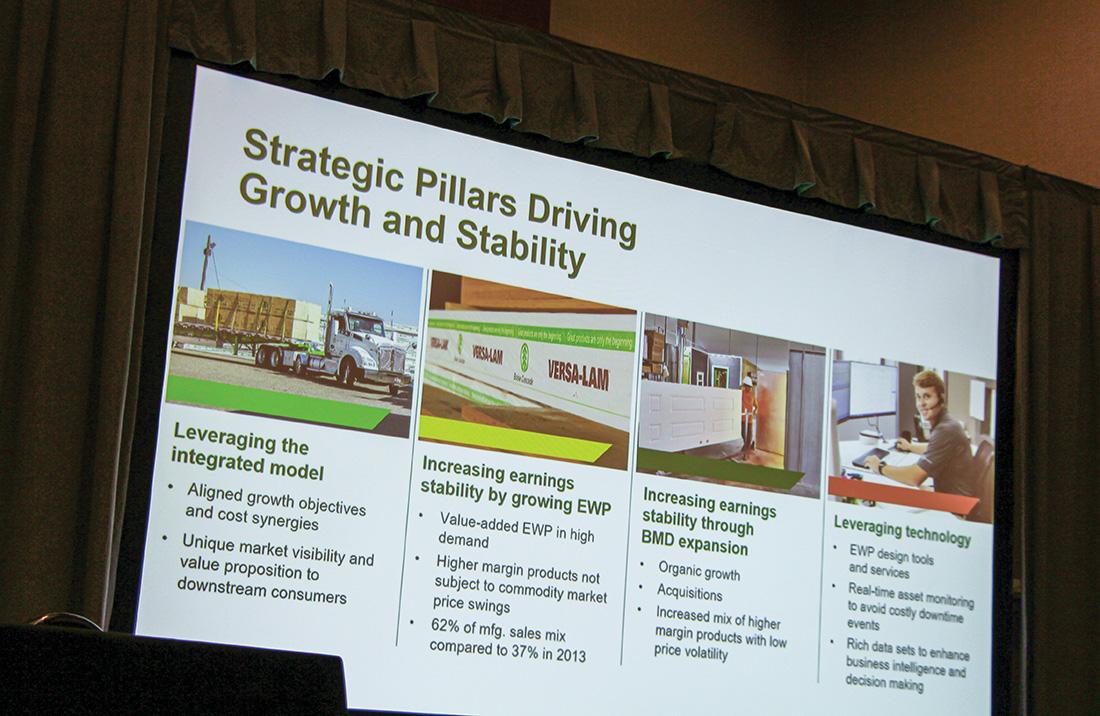

Roseburg: Billion-Dollar Investments, Tight Execution

Fresh off announcing the restart of construction on a new medium-density fiberboard (MDF) facility in Oregon, Jim Salchenberg of Roseburg detailed a sweeping capital investment strategy.

Fresh off announcing the restart of construction on a new medium-density fiberboard (MDF) facility in Oregon, Jim Salchenberg of Roseburg detailed a sweeping capital investment strategy.

From 2021–2024, the company approved more than 400 projects totaling $1.1 billion, delivering them within 3% of budget despite post-pandemic challenges.

Salchenberg distilled that success into three principles: “Own the budget… protect the scope relentlessly… and never accept ‘it takes what it takes, and it costs what it costs.’”

Engineered Wood: A Structural Shift, Not a Cycle

One of the clearest themes at PELICE 2026 was the accelerating role of engineered wood products (EWP).

One of the clearest themes at PELICE 2026 was the accelerating role of engineered wood products (EWP).

Lofton Beasley of Weyerhaeuser framed the shift in unmistakable terms: “These forces are structural, not cyclical.”

He pointed to long-term changes in construction, including labor shortages, demand for speed and predictability, and increasing reliance on prefabricated systems. These trends are driving adoption of engineered solutions that reduce variability and improve efficiency.

Beasley emphasized that EWP is central to long-term strategy. “The message is clear: EWP is not peripheral. It is a central mechanism for translating timberland strength into durable, higher-return growth.”

Weyerhaeuser is backing that strategy with capacity expansion, including a new TimberStrand facility designed to convert lower-quality logs into higher-value products.

Housing Market Reality: Short-Term Pressure, Long-Term Opportunity

Market analysis from Chris Beard of John Burns Research and Consulting provided a grounded look at demand drivers.

Market analysis from Chris Beard of John Burns Research and Consulting provided a grounded look at demand drivers.

“New construction is the near-term drag,” Beard said, pointing to elevated housing inventory and slower starts. However, the broader picture is more nuanced.

With the median U.S. home now 44 years old, aging housing stock is fueling a surge in repair and remodeling activity—now rivaling new construction in total spending.

Beard highlighted several tailwinds, including rising home equity levels, larger tax refunds supporting renovation spending, and increasing frequency of disaster-related repairs.

While new construction may soften in the near term, Beard said forecasts point to a rebound beginning in 2027.

Market Dynamics: Shifting Materials and Global Pressure

Guillermo Velarde of AFRY Management Consulting outlined broader structural changes across panel markets:

Guillermo Velarde of AFRY Management Consulting outlined broader structural changes across panel markets:

-

OSB continues to gain share due to cost and performance advantages

-

Plywood faces ongoing substitution pressure

-

Particleboard markets are tightening under competition from large-scale European producers

-

MDF investments are ramping up, with new capacity expected to compete more effectively with imports

AFRY’s recommendations focused on operational efficiency, supply chain optimization, and product diversification as key levers for future competitiveness.

In addition to keynote sessions, PELICE 2026 featured deep dives into:

-

Artificial Intelligence in manufacturing

-

Catastrophe and risk management

-

Wood fiber sourcing and optimization

-

Veneer and plywood production advances

-

Fire and safety technologies

-

Mass timber construction

-

Energy use and emissions reduction

A Conference That Still Delivers

Nearly two decades after its launch, PELICE continues to fulfill its original mission: Bringing the industry together to share knowledge, confront challenges, and identify opportunities.

The 2026 event made one thing clear, while markets may fluctuate, the industry is actively adapting through innovation, disciplined investment, and a sharpened strategic focus on engineered solutions.

As Lofton Beasley put it, the forces shaping the future aren’t temporary—they’re foundational.

And based on the energy in Atlanta, the industry is ready to meet them head-on.

2026 PELICE Daily Recaps

Inside the 2026 PELICE Expo

THE TENTH ONE

Before the very first Panel & Engineered Lumber International Conference & Expo, the organizers wrote: “We hope your participation provides you inspiration and education, as well as some relief if your markets are slumping. But no matter the market condition, the show must go on, education must continue, and when the tide turns for the better, you will have taken full advantage. There is no better place at this moment in time to obtain a true collective understanding of the many segments of the panel industry.”

Before the very first Panel & Engineered Lumber International Conference & Expo, the organizers wrote: “We hope your participation provides you inspiration and education, as well as some relief if your markets are slumping. But no matter the market condition, the show must go on, education must continue, and when the tide turns for the better, you will have taken full advantage. There is no better place at this moment in time to obtain a true collective understanding of the many segments of the panel industry.”

That was in the spring of 2008. We’re of course now in the spring of 2026. Many of those earlier written words ring true again today, but in reality the economy was a lot worse at that time, and getting “worser” by the day (hello subprime mortgage crisis). Probably the only time it got even worse was during COVID, but that didn’t last too long, and then the post-COVID boom knocked everyone’s socks off. Through it all, today, there is still no better place, than PELICE, to gain a “collective understanding” of the current state of the panel industry.

And that’s always been the intention of PELICE—to provide the latest snapshots of the economy and building markets, the latest in mill projects, the latest developments in equipment and technologies, the latest trends in producer company cultures, and much more. And indeed the show has gone on through these years, more specifically every other year, through four presidents no less, and here we suddenly land at the 10th PELICE.

Sure it’s a major milestone, but then again there are producer and vendor companies involved in this PELICE who have been around 80-90-100 years and more. In that context, PELICE is still but a youngster.

In its nearly 20 years duration, PELICE has been a positive contributor to the panel and engineered wood products industry. That’s really what it set out to be.

See you in Atlanta.

Latest Show News

Perfect 10 Exhibitors At PELICE

The recent Panel & Engineered Lumber International Conference & Expo (PELICE), held in mid-April at the Omni Hotel in Atlanta, was the 10th PELICE since its inception in 2008. Event hosts Panel World magazine and Georgia Research Institute...

PELICE 2026 in Atlanta: Industry Leaders, Big Investments, And A Clear Path Forward

The 10th Panel & Engineered Lumber International Conference & Expo (PELICE) lived up to its reputation as a can’t-miss industry event, bringing 470 attendees, 95 exhibitors, and 41 speakers to Omni Atlanta Hotel at Centennial Park on April 16–17....

April 6-7, 2028 | Atlanta, Georgia

PELICE is the Educational Event for the Worldwide Wood Products Industries Including Veneer, Plywood, OSB, MDF, Particleboard, Engineered Wood Products, Mass Timber and Value Added